The Exchange Magazine – 2021

We are excited to bring you the latest edition of the Exchange Magazine.

2021 Edition

Click here to read

We are excited to bring you the latest edition of the Exchange Magazine.

2021 Edition

Click here to read

Hi Members,

Hope everyone is doing well in what no doubt has been a busy last couple of months in the FY changeover period. Not to mention the extraordinary time we are in!

At FTA our focus is on continuing to deliver CPD and other services to you digitally during this lockdown/WFH time. Our calendar is full as you will see from webinars and our other programs such as Treasury Management and Fundamentals. Please keep looking out for these, continuing professional development is something that is never not needed.

The big thing right now though is the work on Conference. Hopefully, you’re all seeing our updates, we’re extremely proud of, and excited by, the program that has now been developed. When we have speakers of the caliber of Kevin Rudd, Stephen Koukoulos, and Matt Gertken, and case studies from businesses such as Coles and Oil Search, you know its going to be great.

Please jump on board, we can’t wait to see everyone there – the interaction and networking is also fantastic on our platform.

Take care

Ben Leaver

It has been an honour to be the first female Chair of the Young Leaders Committee for the FTA. The opportunity to collaborate with and work alongside such a high caliber of young professionals in the Treasury industry has been both rewarding and fulfilling.

What I enjoy about being part of this Committee is the immense talent, diversity of skills, and strong work ethic each member shares, tantamount to their professional careers and development.

Our committee has worked successfully towards our FY20 objectives of educating our local students and empowering young professionals in our industry to aspire to succeed in their career – which is what makes me truly proud of being part of the FTA community.

Therefore, I would like to extend my special thanks to Kirsty, Toby, Andrew, and Piero for all your tremendous efforts and commitment over the past year. I have been thrilled to participate in and observe the development of this committee, as we aspire towards becoming future leaders in the Corporate Treasury and Finance space in Australia.

When I first began my journey in the FTA community, I was extremely lucky to be part of the mentorship program as a mentee. Notwithstanding my previous experiences of mentorship programs earlier in my career in Banking, I was able to really distinguish and relate to the philosophy of mentorship. The FTA matched me with an influential Corporate Treasurer as my mentor. I recall feeling immediately impressed not just by her successful career, but most importantly her passion in fulfilling her role as a devoted mother and having such a warm bubbly personality! I was inspired instantly and understood that was the same magnitude of energy and presence I would like to demonstrate as a future mentor.

Over the past year attending educational FTA seminars, networking events, webinars, and conferences it has been such a rewarding experience since I joined the Association. These opportunities in meeting incredible professionals in the corporate industry have created lasting impressions as I continue to support and advocate the Treasury Profession.

Despite the immediate global challenges this year, the Young Leaders Committee has committed to keeping us at the forefront of this dramatically evolving environment. With a variety of concerning the industry, risks have never been so prevalent that the reliance on sound Finance and Treasury professionals has never been so demanding.

Our aim is to continue to empower young professionals, aspiring students as well as the rest of our Treasury community to continue to strive for excellence in their current and future careers, as well as their corporate service – We, will continue to promote our committee in FY21 through the communication of our innovative ideas, collaboration with our extensive FTA network, and ultimately demonstration of our financial stewardship through our industry experience.

I look forward to seeing the YLC continue to develop and contribute exciting outcomes to the FTA community in the coming Financial Year.

Mary-Jane Carcasona

Have you seen and explored the new Member Portal? Behind the scenes, we have been working hard to bring you a more streamlined and Member friendly portal. Included in the recent upgrades has been the inclusion of a Member Forum for the Australian Treasury Community.

Ask questions, or create a new discussion thread. The Member Forum is the place to engage with the Australian Treasury Community.

How to Subscribe –

You can choose to receive an update each time a comment is made in all Forum Threads by clicking ‘Subscribe for new topics’ found on the Forum Home Page, under Finance & Treasury Associaiton (as above); alternatively you can select which Threads you only wish to receive updates from by clicking on your chosen Thread (eg General Treasury) and clicking on ‘Subscribe for new topics’.

If you would like to create a new Topic, you can do this by selecting ‘Add topic’ in the top right corner of your chosen Thread.

We encourage you to sign in and join the conversation here.

Webinar: Bank Treasury – 23rd September

University of Western Australia Event – 24th September

Webinar: Supply Chain Finance: An Australian Perspective – 30th September

Treasury Management Course – 15th, 22nd, & 29th October

Fundamentals of Treasury Course – 27th October

National FTA Conference – 10th, 11th, & 13th November

In November the inaugural virtual FTA Conference 2020 is taking place. I have been involved in a number of FTA conferences over the years and it has been inspiring to work on this initiative, helping the FTA executives and the conference committee pull together an event creating an opportunity to enjoy all the benefits of attending a conference as we have shared in the past, this time virtually. I am excited we will have the benefit of a virtual conference which will not be a series of webinars, but an opportunity to hear presentations, interact with panels (many of who will be on a live stage), have one on one sessions with our exhibitors, and our peers.

Even though we have been put in a position to run the conference in this way, due to the COVID-19 pandemic, the outcome is an opportunity to have an event where we can reach an even greater audience than has been possible in the past. Yes, the networking will be different, but it will be there, it will be an opportunity to share the stories and experiences that enrich our attendance. The conference committee has pulled together a technical program that is packed full of content and insights from your treasury peers (over 20 corporate treasurers supported 22 experienced treasury professionals) by sharing their experiences while developing a view on what the future of treasury may look like. This is complemented by our inspirational/experienced speakers focusing on economics, global relations, the outcome of the US elections and our future. Finally, I must, in advance, thank our sponsors and exhibitors, they are making a contribution to the content, offering virtual experiences, and providing support in a number of other ways.

Book your place today – www.ftaconference.com.au

Regards,

Paul Travers

Do you have an upcoming role you need to advertise? We’re pleased to offer companies the chance to promote their new listings on the FTA jobs board. Find out more by contacting us at membership@financetreasury.com.au

We have recently changed our mailing address and contact phone number. Please ensure you have also updated your records to ensure your communications to the Association are received in a timely manner.

PO Box 21003

Little Lonsdale Street

Melbourne VIC 8011

Australia

+61 (03) 9132 5240

![]()

![]()

![]()

3 October 2019

Aidan Shevlin, CFA

Head of Asia Pacific Liquidity Fund Management

J.P. Morgan Asset Management

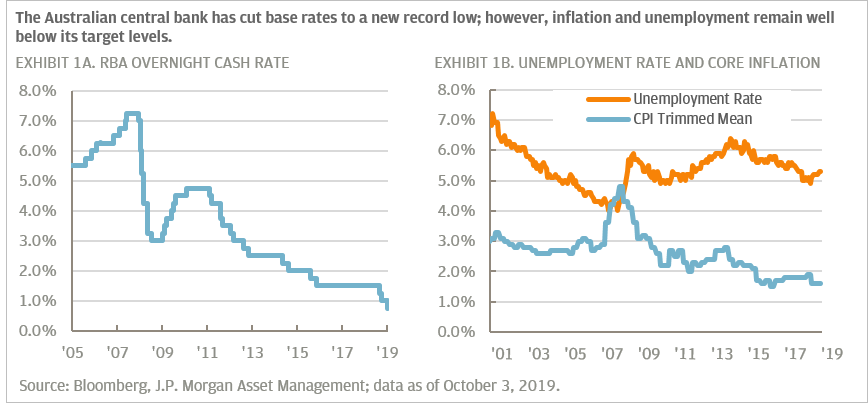

At the beginning of October, the Reserve Bank of Australia (RBA) cut its overnight cash rate by 25bps to a new record low (Exhibit 1a). The third rate cut in five months has effectively halved the central bank’s key policy rate – leaving the RBA in uncharted territory and one step closer to unconventional monetary policy to achieve potentially unattainable employment and inflation goals. The current trajectory of cash rates will have significant and far-reaching implications for local currency cash investors.

Optimistic rate cuts

In recent speeches, RBA governor Philip Lowe struck an upbeat tone, noting the economy had reached a “gentle turning point”1 helped by a combination of low interest rates, tax cuts, lower currency, infrastructure spending and housing market stabilization.

Despite this professed optimism, the RBA still cut rates in October and remained dovish, committed to “ease monetary further if need to support sustainable growth in the economy, full employment and the achievement of the inflation target”2. However, given current lack of macroeconomic drivers to achieve the central banks full inflation of 4.5% was last reached in 2008 and core inflation target of ≥2% (Exhibit 1b), the probability of attaining either goal remains remote.

The reality is more nuanced: While Australia is currently in its 28th year of economic expansion, gross domestic product (GDP) growth has slowed to a decade low; moreover the rising participation rate is offsetting almost 2-years of positive jobs creation and despite the recent recovery, housing prices have fallen below their long-term trend. Meanwhile, the long term slowdown and rebalancing of the Chinese economy will eventually weigh on exports – although short-term Chinese infrastructure stimulus will benefit Australia’s commodity driven economy.

Sluggish consumption and structural trends

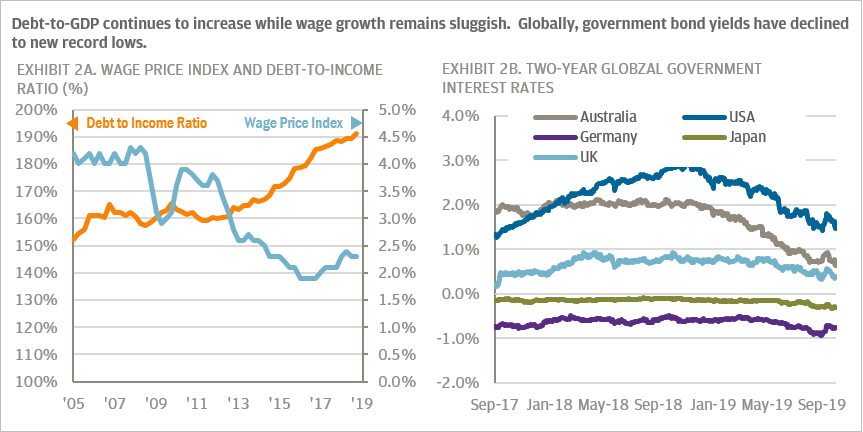

Apart from weak global growth, the RBA’s other key domestic concern remains the lack of growth in domestic consumption – especially during a period of rising employment. However, this can partly be explained by job insecurity, muted wage growth and the high level of consumer indebtedness (Exhibit 2a). All these factors should still benefit from lower interest rates – suggesting that monetary policy remains an effective policy tool – provided commercial banks pass the rate reductions on to consumers.

Interestingly, for the first time, the RBA alluded to a new rationale for the latest rate cut. The structural shifts in global interest rates (Exhibit 2b) – which have fallen to record lows have also placed downward pressure on Australian interest rates. The central bank fears if it ignored the actions of major central banks, the “exchange rate would appreciate, which in the current environment would be unhelpful on terms of achieving both the inflation target and full employment”3.

The implications of sustain lower interest rates

The recent rate cuts, fiscal stimulus and continued Chinese commodities demand, suggest the modest Australian economic recovery is likely to endure. However, growing expectations of additional monetary policy easing by major central banks may force additional, unnecessary RBA rate cuts and even trigger unconventional monetary policy to restrain unwanted capital inflows and AUD appreciation.

For Australian cash investors who are more familiar with high interest rates, steep yield curves and competitive deposit rates, the prospect of extremely low or even zero yields represents a significant challenge. These difficulties have been compounded by the Royal Commissions impact on commercial banks demand for deposits and the Australian Prudential Regulatory Authority’s (APRA) clarification on the definition of cash.

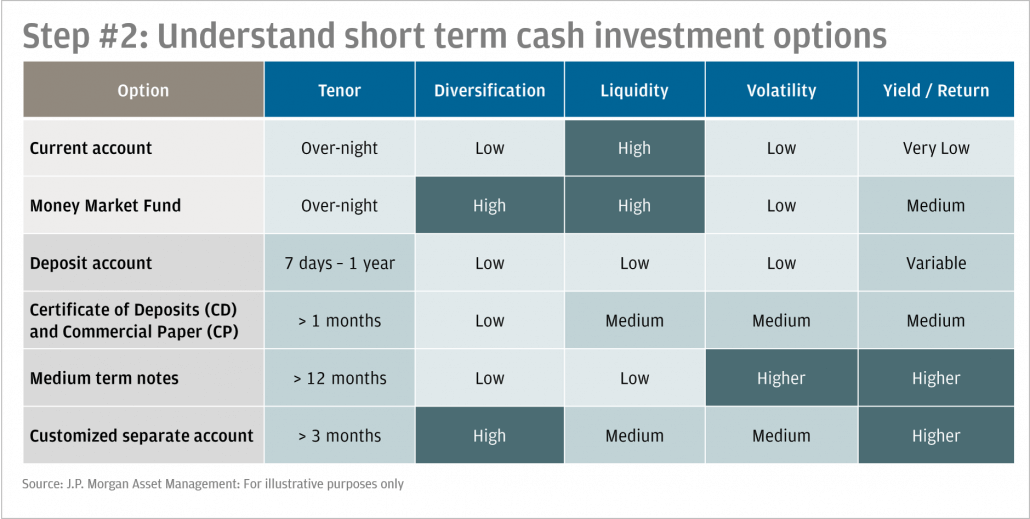

Nevertheless there are several techniques developed and refined during the past decade of zero US interest rates which should help Australian corporate treasurers mitigate some of these complications. These include diversifying beyond deposits into money market funds and ultra-short duration funds, segmenting cash by liquidity requirements and identifying sectors and tenors that offer additional return for minimal reductions in liquidity and security.

Although combining these three techniques will not fully offset the negative impact of RBA rate cuts on cash returns, they will allow treasurers to achieve a competitive return consistent with the objectives of capital preservation and maintaining a high degree of liquidity.

To read more our liquidity insights, visit www.jpmgloballiquidity.com

1 An Economic Update by Philip Lowe; as of September 24, 2019

2 Statement by Philip Lowe, Governor: Monetary Policy Decision; as of October 1, 2019

3 An Economic Update by Philip Lowe; as of September 24, 2019

The definition of cash, while ostensibly straightforward – banknotes and coins – becomes increasingly challenging when the demands for higher returns counteracts the obligation to ensure adequate liquidity and the commitment to avoid losses.

As memories of the liquidity stress and market dislocation triggered by the global financial crisis faded, the range of financial instruments deemed acceptable in Australian cash products broadened dramatically. This was also a time when investors grappled with the challenges of outperforming attractive headline retail bank deposit rates.

Unfortunately, defining which instruments are truly cash equivalents is one of the most difficult tasks for modern corporate treasurers.

The Regulatory Dilemma

Globally, cash investors look to regulators and rating agencies to define and clarify suitable cash investment instruments and structures. This is especially true in the United States, European Union, and China, where the size and systemic importance of liquidity and money market funds (MMFs) made this a critical regulatory issue following the 2008 financial crisis.

These rules and regulations vary from prescriptive, listing specific approved and unapproved instruments, to abstract, outlining key sources of investment risk and limits to mitigate them. Regardless of the regulator’s philosophy, the ultimate goals remain the same – to ensure adequate liquidity and minimise the probability of losses. Over the past decade, global regulators have strengthened MMF guidelines. They now demand higher levels of liquidity, impose tighter investment limits and require increased diversification. For both retail and institutional investors, these new rules have raised the standard of MMF investing while significantly reduced the likelihood of funds suffering losses, albeit at the expense of lower potential returns.

In contrast to detailed global standards, Australian regulators have historically demurred the responsibility to define cash or the suitability of various instruments for cash investments. The Federal government’s unlimited bank guarantee during the Global Financial Crisis helped shelter the local financial industry while a long history of self-regulation encouraged investors to create their own definitions of cash and cash equivalents.

However, in 2018, a review of cash investment products by the Australian Prudential Regulation Authority (APRA) raised significant concerns about the level of volatility and risk in these products. Across the industry, the range of instruments and structures defined as cash varied enormously – as did returns. This created confusion for retail and institutional investors. In its subsequent report, APRA highlighted “examples in the industry where cash investment options appear to include exposure to underlying investments that would not generally be considered cash or cash-like in nature”1.

To encourage investment consistency and reduce the volatility of cash investment products, APRA concluded that “cash equivalents represent short-term, highly liquid investments that are readily convertible to known amounts of cash and which are subject to an insignificant risk of changes in value”1.

Cash means security, liquidity and return

The report signalled a tougher regulatory stance and additional focus on questionable cash investments styles. However, in the absence of detailed regulatory guidelines and exact definition of liquidity and risk, investor due diligence is still required to balance the need to preserving capital, while ensuring suitable levels of liquidity and maximising returns.

Three key steps in this process involve clarifying investment policies, creating well defined investment objectives and implementing cash segmentation.

Firstly, using an investment policy statement forms a solid foundation for cash investment decisions. A well written policy provides clarity, instils discipline and allows the organisation to successfully navigate shifting markets, changing regulations and evolving business needs.

Secondly, by defining short term investment objectives and the strategies for achieving them, an organisation can establish acceptable levels of risk, identify permissible investments and detail relevant constraints.

Finally, by putting cash into different segments, the organisation can optimise its investment choices – ensuring it has sufficient liquid cash to meet its daily needs while avoiding the opportunity costs associated with very high levels of liquidity and principal protection by diversifying across different types of cash investment depending on their level of liquidity, volatility, and diversification.

In Conclusion

The new APRA definition of cash has already prompted a significant reorganisation across the Australian cash management industry with several instrument structures being avoided and more conservative investment guidelines introduced. This, combined with more due diligence and understanding of the underlying risks by retail and institutional investors, should help the industry create a safer foundation for future growth.

To read more our liquidity insights, visit www.jpmgloballiquidity.com

Copyright © 2024 The Australian Corporate Treasury Association | ABN: 70 006 509 655

DON’T DELETE